Buying a car feels like a milestone of adulthood. It symbolizes freedom, mobility, and independence. You imagine yourself rolling down open roads, music up, windows down, without a care in the world.

What you don’t imagine is how your car slowly begins to eat into your bank account. It happens silently and relentlessly. This occurs day after day, month after month.

Car ownership is one of the most underestimated financial commitments people make. We assume the main expense is the price of the car itself. We think once we have signed the papers and driven home, the money part is basically handled. But a car is not a one-time purchase. It is a long-term relationship with financial obligations that keep arriving, even when the car is just sitting still.

A vehicle costs money to run, to park, to maintain, and astonishingly even to simply exist. Here is the full story of the true cost of driving, along with strategies to minimize those hidden expenses.

Silent Loss Depreciation

Depreciation is the largest cost of car ownership, and the one most drivers overlook. The moment a new car leaves the dealership, its value drops dramatically.

Within the first year, it can lose up to 20 percent of its worth. Within five years, it may lose nearly half. Even with impeccable care, the market decides that newer always means better.

One way to avoid this steep hit is to buy a lightly used, well-maintained vehicle instead of a brand-new one. This approach allows you to skip the bulk of the initial depreciation while still enjoying a reliable car.

Fuel: The Daily Drain

Fuel costs feel routine, but they accumulate rapidly. Commuting, errands, weekly outings and spontaneous trips all require fuel, and global prices fluctuate unpredictably.

Even with fuel-efficient vehicles, filling the tank is a recurring financial hit many underestimate.

Choosing a car with better fuel efficiency can significantly reduce this ongoing burden. Opting for a smaller engine or even a hybrid system can also help.

Additionally, planning trips efficiently, combining errands, or using public transit for shorter journeys can cut mileage and, consequently, fuel expenses.

Maintenance and Repairs

Routine maintenance is essential to keep a car running safely. Oil changes, brake pads, fluid replacements, and tire rotations become a recurring part of life.

The older the vehicle, the higher the risk of unexpected repairs. These range from a warning light that signals a failing part to an expensive mechanical breakdown.

Preventative maintenance is not just practical, it is a way to save money. By keeping up with scheduled service, you reduce the likelihood of costly emergency repairs. Similarly, shopping around for quality repair services and comparing prices for parts can prevent bills from skyrocketing.

Parking and Tolls

Urban living transforms parking into a premium commodity. Monthly parking fees, residential permits, and short-term paid parking can quickly add up.

In addition, tolls on bridges, highways, and tunnels can feel like a tax for every trip you take. Planning routes in advance, seeking less expensive or residential parking options, and consolidating trips can help reduce these costs.

In some cities, car-sharing arrangements or choosing neighborhoods with better parking availability can also significantly ease this burden.

Insurance: The Price of “What If?”

Insurance is unavoidable, and premiums are influenced by location, driving record, age and the type of vehicle. Even with coverage, deductibles mean that drivers still pay a significant portion of repairs themselves.

Compare providers regularly. Update policies to reflect your current driving situation. Raise deductibles when financially safe. These actions can lower costs without sacrificing protection. For some households, switching to a car that has lower insurance premiums or bundling policies can also yield substantial savings.

Registration and Taxes

Annual or periodic fees for registration, emissions testing and road taxes are mandatory. While individually small, they add up over time.

Choosing a vehicle with lower annual fees or that meets the highest emissions standards can reduce the cost of compliance. Staying aware of renewal deadlines also avoids late penalties, which are essentially wasted money.

Tires, Cleaning and Accessories

Tires wear down constantly, and replacing them is unavoidable. Seasonal changes often require additional sets, and premium tires carry a premium cost.

Buy tires off-season. Select reputable but cost-effective brands. Keep them properly aligned and rotated to extend their life. This minimizes expenses.

Similarly, car washes, detailing, and optional accessories are not strictly necessary. Prioritizing functionality over aesthetics can prevent money from leaking away unnecessarily. Treating your car as a tool rather than a status symbol can save thousands over the years.

The Psychology of driving and spending

Cars encourage behaviors that increase costs. We drive more. We explore distant stores. We justify additional purchases simply because we have the means to do so.

Being consciously aware of these patterns can help. Track expenses diligently. Limit unnecessary trips. Evaluate the real cost before buying non-essential items. These actions can help curb the financial impact. Even considering whether one car is sufficient for a household can reduce all associated costs dramatically.

Owning a car unlocks opportunities and convenience that few are willing to give up.

The freedom to travel on your own terms is valuable, but it comes at a significant and ongoing cost. Understanding the hidden financial realities is essential. Take proactive steps to reduce these costs. Transform car ownership from a silent drain on your resources into a manageable, predictable expense. Buying used, maintaining your vehicle, driving efficiently, managing insurance and parking, and making conscious choices about accessories and lifestyle are all ways to keep costs under control. A car may take you wherever you want to go, but it should not be the thing that keeps you from getting ahead.

South Africa’s economy holds a paradoxical place in the world. It’s one of the most developed and diversified economies on the African continent. Yet, its potential is persistently undermined by deep structural fragilities.

South Africa is rich in mineral resources. It also has a sophisticated financial system and a strong industrial capacity. These elements have long led to South Africa being viewed as a continental economic anchor.

But beneath the surface, chronic challenges hinder growth. These include crippling power shortages, high inequality and a fragile fiscal position. These issues weigh on investor confidence and limit the country’s ability to deliver broad-based prosperity.

Illustration 1: Flag of South Africa

To understand South Africa’s economic trajectory, one must explore its dual identity. It is a resource-rich, relatively advanced emerging market. However, it struggles to convert its potential into sustained, inclusive growth. The legacy of apartheid, spatial inequality, and state-owned enterprise mismanagement continues to cast a long shadow. Meanwhile, the government is pursuing reform.

Today, South Africa stands at a crossroads. It could leverage its natural endowments, human capital and reform momentum to enter a new growth phase. Alternatively, it might remain stuck in a low-growth equilibrium, unable to overcome its systemic constraints.

The following article will explore South Africa’s macroeconomic performance, structural strengths, institutional weaknesses and long-term opportunities. We will weave together the latest economic data, reform trends and risk factors. These elements will determine whether South Africa can unlock its promised future.

History and Foundations

Pre-Colonial and Colonial History

Before European colonization, indigenous communities such as the Zulu, Xhosa, Sotho, and Tswana had well-established systems of agriculture.

They practiced pastoralism and trade. Cattle ownership, artisanal crafts, and local trade networks formed the backbone of their economies. These societies demonstrated significant economic organization and regional exchange, long before colonial influence reshaped the subcontinent.

European settlers arrived and began a significant change in South Africa’s economy. The Dutch arrived first in 1652. Later, the British followed. Colonization introduced formal property systems, trade oriented toward European markets and the appropriation of land from indigenous populations.

The establishment of the Cape Colony and subsequent British expansion laid the foundation for a dual economy. This favored European settlers. It systematically excluded Black South Africans from wealth creation, land ownership, and political participation.

Discovery of Gold and Diamond

The discovery of diamonds in Kimberley in 1867 began South Africa’s transformation.

Gold was then found in the Witwatersrand in 1886. This discovery turned the nation into a mining powerhouse. These discoveries attracted massive domestic and foreign investment and spurred rapid urbanization.

Mining became the primary driver of the economy, stimulating infrastructure development such as railways, ports and telecommunication networks.

However, it also entrenched social and economic inequalities. The system relied heavily on migrant labor. It drew men from rural areas under harsh conditions to work in mines. Wealth accumulated by mining magnates fueled industrial expansion but remained concentrated within a small elite.

Illustration 4: Image showing Cape Colony in the 19th century.

Industrialisation and Apartheid

Industrialization during the late 19th and early 20th centuries diversified the economy. Manufacturing sectors such as textiles, food processing, and metalwork emerged alongside mining. The formation of the Union of South Africa in 1910 enabled national coordination of infrastructure and economic policy. Protective tariffs encouraged local manufacturing, but mining exports remained central, exposing the economy to global commodity fluctuations.

The formalization of racial segregation, culminating in apartheid after 1948, profoundly shaped the structural foundations of South Africa’s economy.

The Land Acts of 1913 and 1936 confined Black South Africans to underdeveloped “homelands.” These policies restricted their participation in high-value sectors. Pass laws regulated labor mobility to ensure a steady supply of cheap labor for mines and urban industries. The state supported industrial growth primarily for white-owned businesses.

Black South Africans were largely excluded from ownership. They lacked access to credit and skilled employment. Despite this, industrialization advanced in several areas. Notably, it progressed in energy, transport, and urban manufacturing hubs. This development created a modern industrial base, even within a deeply unequal society.

The late apartheid period brought additional pressures, including international sanctions, divestment, and internal resistance. The economy relied increasingly on mechanized mining, state-owned enterprises and financial markets to maintain growth.

At the same time, rising labor unrest and political instability highlighted structural weaknesses. These inequalities would become central challenges for the post-apartheid era.

The transition to democracy in 1994 marked a turning point. The ANC-led government inherited an economy with advanced infrastructure. It had a strong industrial base and a sophisticated financial sector. However, there was also severe inequality, underdeveloped rural areas, and limited human capital among the majority population.

Early reforms included the Reconstruction and Development Programme (RDP). The Growth, Employment and Redistribution (GEAR) strategy also aimed to balance social redress. They pursued macroeconomic stability. They opened South Africa to global trade and foreign investment. These reforms also addressed long-standing inequities.

Modern South Africa

Today, South Africa’s economic structure reflects this layered history. It features a modern, globally integrated industrial and financial sector.

The economy of South Africa is currently the largest economy in Africa as of October 2025. It is a mixed economy, emerging market and upper-middle-income economy, and one of only eight such countries in Africa.

Cape Town is SA’s second-largest city by population. It serves as Africa’s tech hub and has a large startup community. The city is popular among digital nomads. The city is home to hundreds of tech firms, and is referred to as the “Startup Capital of Africa”.

However, there are persistent inequalities. A dual labor market exists, along with uneven development between urban and rural areas.

South Africa levies a top personal income tax rate of 45%. It also imposes a corporate tax rate of 27%, alongside value-added and capital gains taxes. This results in an overall tax burden of about 23.4% of domestic income.

Key Industries and Sectors

Mining and Natural Resources

Mining has historically been the backbone of South Africa’s economy, shaping its industrialization, urbanization, and global trade presence. Diamonds were discovered in Kimberley in the late 19th century. This event, followed by the gold rush in the Witwatersrand, established South Africa’s mineral wealth as a global mining powerhouse.

Mining has created employment opportunities, generated export revenue, and funded infrastructure development. Platinum, gold, diamonds, coal, manganese, and chrome remain critical exports. South Africa accounts for a significant share of global supply, especially in platinum and manganese.

In 2019, South Africa ranked among the world’s leading producers of several key minerals. It was the largest global producer of platinum, chromium, and manganese. The country was the second-largest producer of titanium. It was also the third-largest producer of vanadium.

The country also held prominent positions in other sectors. It was the 6th-largest producer of iron ore. It ranked as the 11th-largest producer of both gold and cobalt. It was the 15th-largest producer of phosphate. In 2018, South Africa was the world’s 12th-largest uranium producer.

However, the sector faces mounting structural challenges. Ore quality is declining, making extraction more expensive and technologically demanding. Deep-level mining, particularly for gold, involves complex engineering and escalating safety concerns.

Analysts warn that without substantial reinvestment in technology and workforce training, key operations could become economically unviable within decades. Rising operational costs, coupled with fluctuating global commodity prices, place additional pressure on profitability.

Illegal mining, locally referred to as “zama zamas,” presents a parallel challenge. These informal operations not only undermine formal mining companies by diverting resources. They also reduce legal production volumes.

Additionally, they exacerbate safety risks, cause environmental degradation, and complicate regulatory enforcement. Mining companies face significant difficulties navigating bureaucratic delays in permits and licenses. Environmental compliance adds to these issues. These challenges further discourage both domestic and foreign investment.

Environmental and social pressures are also growing. Mining is energy-intensive, water-intensive, and environmentally disruptive, and South Africa faces heightened scrutiny regarding sustainable practices and social responsibility.

Illustration 10: Gold from a Zama Zamas

Communities around mines demand benefits and fair labor practices, while environmental groups emphasize rehabilitation and water management. Transitioning to sustainable mining practices is essential. Adopting modern technology is necessary. Addressing labor and regulatory challenges is crucial if the sector is to remain a pillar of the economy

Mining’s share of South Africa’s GDP has declined from 21% in 1970 to just 6% in 2011. However, the sector continues to dominate the country’s export profile. It accounts for nearly 60% of total exports. Mining also contributes approximately 9% of the nation’s value added.

The industry is anchored by some of the country’s largest and most influential companies. These include Anglo American, one of the world’s leading diversified mining firms. Sibanye Stillwater is a major producer of gold and platinum group metals. Impala Platinum is a top global platinum miner. These companies not only drive significant export revenue but also shape employment, technological innovation, and investment patterns within the sector.

South African Agriculture

Agriculture plays a modest but important role in South Africa’s economy. It formally employs around 5% of the workforce. Additional work is provided through casual and seasonal labor.

The sector contributes approximately 2.8% to national GDP. This is a relatively low share compared to other African countries. However, its social and economic significance extends beyond these figures.

It supports rural livelihoods, food security, and exports. South Africa is a leading exporter of fruit, wine, nuts, and sugar. Its agricultural products, like wine and citrus, reach premium markets globally.

The sector provides employment in rural areas and is essential for community stability, especially where alternative economic opportunities are scarce.

South Africa is a major global producer of a range of agricultural products. In 2018, the country produced 19.3 million tonnes of sugarcane, ranking 14th worldwide; 12.5 million tonnes of maize, the 12th largest globally; 1.9 million tonnes of grapes and 1.7 million tonnes of oranges, both 11th largest; and 397,000 tonnes of pears, the 7th largest producer in the world.

Beyond these staples, South Africa ranks among the top global producers of several other crops. These include chicory roots and grapefruit (both 4th), cereals (5th), and green maize and maize (7th). Additionally, castor oil seed and pears rank 9th. Sisal and other fiber crops are ranked 10th. Despite its strengths, the sector faces significant challenges, including increasing foreign competition and persistent crime affecting farms.

Farm attacks, in particular, have sparked debate over government intervention. Some critics argue that authorities either over-prioritize this issue or under-prioritize it relative to other forms of violent crime.

Furthermore, agriculture is increasingly vulnerable to climate change, including droughts, shifting rainfall patterns, and water scarcity.

Illustration 13: Land reform continuous to be a very controversial topic in South Africa. Image from: A fresh approach to land reform

Land reform policies, though critical for historical redress, create uncertainty over tenure and investment incentives, slowing modernization and mechanization. Rural infrastructurelm including irrigation systems, transport networks and storage facilities, requires significant development to improve productivity and competitiveness.

Investments in climate-resilient practices, sustainable irrigation, and agro-processing can enhance the sector’s economic impact while addressing social imperatives.

Manufacturing and Industry

South Africa’s industrial sector is diversified. It encompasses downstream mineral processing, automotive manufacturing, and chemicals. It also includes food and beverage processing, machinery, and construction materials.

The manufacturing sector plays a modest role in South Africa’s economy, accounting for approximately 13.3% of employment and contributing around 15% of GDP. Certain segments of the industry are experiencing growth, including advanced sectors such as aerospace and space technology.

While labor costs remain relatively low compared to developed economies, they are higher than in many other emerging markets. At the same time, expenses for transport, communications, and general living add to the overall cost of doing business. These costs present challenges for competitiveness. They also hinder expansion within the sector.

The automotive sector, in particular, is a significant exporter. It employs thousands in assembly plants for both domestic consumption and global markets. The country is also a hub for automotive manufacturing.

It hosts production plants for major global companies. These include BMW, Ford, Volkswagen, Daimler-Chrysler, General Motors, Nissan, and Toyota. Companies producing in South Africa enjoy benefits from relatively low production costs.

They gain preferential access to new markets through trade agreements with the European Union and the Southern African Development Community. Chemical production, steel and ferroalloy processing, and other industrial activities complement mining, creating an interconnected industrial ecosystem.

Despite these strengths, the sector faces persistent constraints. High electricity costs, largely driven by reliance on Eskom’s aging coal-powered generation fleet and inconsistent supply, create uncertainty for manufacturers.

Power outages and load shedding disrupt production schedules, reduce output, and erode investor confidence. Logistical bottlenecks, including underdeveloped rail systems, port congestion and inadequate road maintenance, further hinder competitiveness, particularly for export-oriented firms.

Illustration 15: South African roads present a challenge for export-driven businesses.

The regulatory environment is intended to protect labor and consumers. However, businesses often cite it as cumbersome and inconsistent. This increases compliance costs and reduces agility. Many manufacturing firms operate at a scale below global competitors.

This limits their ability to achieve economies of scale. It also hinders their capacity to innovate or compete on price. Reforming state-owned enterprises (SOEs) is crucial. Investing in transport infrastructure is also essential. Additionally, reliable energy provision is needed. These actions are widely recognized as prerequisites for revitalizing industrial capacity.

Emerging industrial opportunities exist in high-tech manufacturing, advanced materials and agro-processing. South Africa can leverage its mining expertise in these industries. It can also use its engineering capabilities and research infrastructure. However, realizing this potential requires consistent policy support, streamlined regulation and investment in skills development and technology adoption.

Tourism

Tourism significantly impacts South Africa’s economy. It contributes to both GDP and employment. It also showcases the country’s rich natural, cultural, and historical assets.

South Africa offers a diversity of experiences. The iconic Table Mountain and Cape Town’s vibrant urban culture. The wildlife-rich Kruger National Park. Each destination attracts millions of visitors each year.

The scenic Drakensberg mountains further enhance its appeal. The tourism industry supports a wide range of jobs. This includes hospitality, travel services, transportation, and cultural attractions. These are particularly important in regions where other employment opportunities are limited.

South Africa is renowned for wine tourism. It is also famous for its culinary attractions. The Cape Winelands region is a major draw for international visitors. However, the sector faces several challenges. These include seasonal fluctuations, infrastructure bottlenecks, and concerns over safety and security. These challenges can influence traveler perceptions.

Exchange rate volatility affects inbound tourism. Global economic trends also play a role. They make the industry highly sensitive to both domestic and international developments.

Despite these challenges, tourism remains a strategic sector for foreign exchange earnings. It contributes to regional development and promotes South Africa’s global brand.

Finance

South Africa’s financial sector is highly sophisticated on the African continent. It boasts a well-developed banking system, capital markets, and insurance sector. M

ajor banks such as Standard Bank, FirstRand, and Absa provide a broad range of services. International institutions operating locally also offer retail, corporate, and investment services.

The Johannesburg Stock Exchange (JSE) is the largest in Africa. It serves as a key hub for capital raising, equity trading, and investment. It connects South African companies with domestic and international investors.

The insurance sector includes firms such as Old Mutual and Sanlam. It plays an important role in risk management. It also contributes to wealth preservation.

The financial sector is highly advanced. However, it faces challenges related to regulatory compliance, cyber-security risks, and ensuring financial inclusion for underserved populations.

Efforts to expand access to banking, mobile finance, and fintech solutions are ongoing. These efforts aim to integrate a broader segment of the population into the formal financial system. The robustness of the financial sector positions South Africa as a regional financial hub.

Informal Economy

The informal economy is a critical part of South Africa’s socioeconomic landscape. It provides employment and income for millions. These individuals are unable to access formal labor markets.

Activities in this sector include street vending, small-scale trade, domestic work, informal transport services, and artisanal production. The informal economy is particularly vital in urban townships and rural areas. It helps sustain livelihoods and supports local communities.

Despite its importance, the sector faces significant challenges. Workers often lack legal protections, access to credit, and social security. They also lack regulatory recognition. This makes them vulnerable to economic shocks. C

rime, market restrictions, and limited infrastructure further constrain informal businesses. The informal economy contributes significantly to household income and local economic activity. It acts as a buffer against unemployment and poverty. This highlights its social and economic importance alongside formal sectors.

Green Energy and Transition

South Africa’s transition to a green economy represents both a challenge and a significant opportunity. The country is rich in critical minerals essential for renewable energy technologies. These include lithium, cobalt, nickel, and platinum group metals.

This positions it to benefit from the global shift toward electric vehicles and battery storage. Strategic investment in these minerals, combined with sustainable mining practices, could create high-value export opportunities and stimulate industrial innovation.

Scaling renewable energy production is central to this transition. Solar, wind, and hydroelectric projects can reduce reliance on coal, mitigate environmental impact, and stabilize energy supply.

Expanding the transmission grid, encouraging private investment, and reforming energy governance are vital to unlocking the green economy’s potential.

According to the OECD, integrating renewable energy could support emissions reduction targets. Electrification of transport and clean-energy industrialization can also create new jobs. These strategies diversify the economy and enhance global competitiveness.

Illustration 20: Solar panels being installed in South Africa.

However, success depends on coordinated policy, regulatory clarity, and investment in human capital. South Africa must address governance bottlenecks.

It also needs to tackle infrastructure gaps and financing challenges. Otherwise, it risks underutilizing its renewable potential. Additionally, South Africa may miss opportunities in the rapidly growing global green economy.

Fiscal Health and Macroeconomics

South Africa’s macroeconomic trajectory has been sluggish in recent years. According to the IMF, growth was only 0.7% in 2023, constrained by persistent power outages and logistical bottlenecks in rail and port operations.

The OECD likewise estimates that economic activity slowed to around 0.6% in 2024, reflecting continued uncertainty and infrastructure bottlenecks.

This weak growth has major implications for fiscal health. Public debt has ballooned: from 31.5% of GDP in 2010 to a projected 77% by 2025, according to OECD data.

The cost of servicing this debt is rising sharply. The OECD estimates that by 2025, interest payments will absorb roughly 5.2% of GDP, a major drain on the state’s ability to fund other priorities. These fiscal pressures limit the government’s capacity to invest in infrastructure. They also hinder investment in education and social programs. These elements are the very levers needed to unlock long-term growth.

At the same time, the IMF notes that inflation has moderated: from around 5.9% in 2023 to an estimated 4.5% in 2024, and the South African Reserve Bank (SARB) responded by cutting interest rates. This easing of monetary policy provides some breathing room, but it is balanced against the risk of weakening fiscal discipline.

South Africa stands out among emerging markets in several areas. Its financial markets are among the most developed on the continent. They offer relatively easy access to capital. The country has competitive business tax rates compared with peers.

Transport infrastructure includes ports, rail networks, and roads. It is generally considered superior to that of many emerging economies, such as India, Brazil, Mexico, and China. However, it still lags behind advanced emerging markets like South Korea and Chile.

Foreign direct investment has historically been strong, at over 3% of GDP in the late 2000s, reflecting international confidence in certain sectors of the economy.

Despite these strengths, South Africa faces structural challenges that hinder its competitiveness relative to other emerging economies. Labour costs are higher than in most peer countries, and the availability of skilled workers is constrained by an underperforming education system.

The country’s domestic market is relatively small, limiting scale advantages that nations like China and India enjoy. Moreover, energy supply has been unreliable, with frequent power shortages affecting industrial output and investor confidence.

Innovation and technology adoption are also slower compared with leading emerging markets. This makes it difficult for South Africa to maintain a high-growth trajectory in advanced manufacturing or tech-driven sectors.

On a more positive note, the country has niche strengths, like in aerospace and space technology. South Africa joined the BRICS group in 2011. This inclusion cemented its position among major emerging economies. It provided increased global visibility and created opportunities for investment.

However, to sustain competitiveness, the country needs to improve education. It must invest in infrastructure and ensure a stable energy supply. Policies should be implemented to enhance innovation and productivity. These measures will ensure the country does not fall behind rapidly developing peers.

Inequality and Social Dynamics

One of the most destabilizing aspects of South Africa’s economic challenge is unemployment, particularly chronic and youth unemployment. The OECD reports that the formal employment rate remains low. Only a relatively small share of the working-age population participates in productive, high-quality jobs.

According to IMF data, the unemployment rate was estimated at 32.8% in 2024. Many young people, especially in marginalized communities, find themselves locked out of labor‑market opportunities. This weak job creation is not just a social issue, it undermines human capital development and limits consumer demand.

Inequality in South Africa is profound and persistent. The World Bank notes a very high Gini coefficient for income. Additionally, a significant portion of the population lives in poverty.

Social grants help to cushion the poorest, but they are not a substitute for meaningful inclusion in economic activity. According to OECD analysis, many of the unemployed rely on social assistance.

The spatial legacy of apartheid remains evident. Many low-income households live far from economic hubs. This distance exacerbates inequalities. It makes labor mobility and access to opportunity difficult.

Illustration 25: Two different neighborhoods in South Africa illustrating the inequality.

State-owned enterprises (SOEs) also contribute to social strain. Governance failures, corruption, and inefficiency within SOEs drain public resources.

Black Economic Empowerment (BEE) is a policy framework in South Africa designed to redress the economic inequalities created by apartheid. However, the program has faced criticism for benefiting a relatively small elite. It has not broadly

In 2002, roughly 62% of black Africans lived below the poverty line. About 29% of coloured and 11% of Indians were also below the poverty line. Additionally, 4% of whites lived below the poverty line. Average incomes have risen unevenly. Black households increased from R6,018 in 1993 to R9,718 in 2008. In contrast, white households rose from R29,372 to R110,195.

Median income grew much less than the mean, showing that wealth gains are concentrated among the richest. The black middle class and wealthy population have expanded despite these challenges. Nearly 40% of the richest 10% are now black.

Land Reform and Land Distribution

Land reform has been a central and highly sensitive issue in South Africa since the end of apartheid. The legacy of racially skewed land ownership continues to shape the country’s social and economic landscape.

Under colonial and apartheid rule, a white minority owned most productive land. In contrast, the black majority was confined to underdeveloped homelands or smallholdings.

The government’s land reform program seeks to address these historical injustices. It does so through three main pillars: land restitution, land redistribution, and tenure reform.

Land restitution provides compensation or returns land to those dispossessed under discriminatory laws. Land redistribution aims to transfer land to historically disadvantaged individuals. Tenure reform secures rights for people living on communal or leased land.

Despite these efforts, progress has been slow and uneven. By 2020, only about 10% of agricultural land had been redistributed. Many beneficiaries struggle with limited access to finance, inadequate infrastructure, and lack of farming experience, which in some cases has led to reduced productivity.

The debate over expropriation without compensation (EWC) has intensified in recent years.

Proponents argue it is essential to accelerate equity. They believe it will empower rural communities. Critics warn that poorly implemented EWC could threaten agricultural output. It might also deter investment and harm food security.

Trade and Global Position

South Africa’s economy is closely tied to global markets, with exports accounting for roughly 30% of GDP.

Minerals dominate its export profile, including platinum, gold, diamonds and iron ore, while automotive manufacturing, agriculture and chemicals also contribute significantly.

Imports are concentrated in machinery, electronics, petroleum, and chemicals. This creates structural dependencies. These dependencies make the economy sensitive to global price fluctuations.

China, the European Union, the United States, and neighboring African countries are South Africa’s main trading partners. China receives a large share of metals and minerals. Germany imports vehicles and machinery.

Regional trade through the SADC supports food and manufactured goods exports. Trade agreements with the EU, AfCFTA, and other partners provide market access and encourage foreign investment.

The South African rand (ZAR) plays a critical role in trade but is highly volatile. The South African Reserve Bank manages inflation and currency fluctuations through monetary policy, but global capital flows often influence outcomes.

Exports remain heavily commodity-based. Metals and minerals contribute around 60% of export revenue. Agriculture accounts for about 10%, and manufactured goods roughly 20%.

Imports are dominated by machinery, electronics, and petroleum. Export-oriented manufacturing hubs and industrial incentives aim to diversify trade. However, reliance on raw materials exposes South Africa to commodity price swings. It also makes South Africa vulnerable to global economic cycles.

Credit Rating

South Africa’s sovereign credit rating is a key indicator of its fiscal stability and investment risk. Moody’s currently assigns the country a Baa3 rating with a negative outlook.

This highlights the pressures from high public debt. The country also faces persistent budget deficits and ongoing support requirements for state-owned enterprises such as Eskom.

Fitch and Standard & Poor’s both rate South Africa at BB+ with negative outlooks. They emphasize structural challenges. These include slow economic growth, high unemployment, inequality, and policy uncertainty.

Historically, South Africa maintained investment-grade ratings in the early 2000s, supported by strong institutions and fiscal discipline. However, repeated downgrades over the past decade show the impact of rising debt, energy constraints, and slow reforms. These issues have increased borrowing costs and affected investor confidence.

The negative outlook indicates that further fiscal deterioration could lead to additional downgrades. Policy missteps might also trigger such downgrades.

On the other hand, successful reforms could stabilize the country’s ratings. Improved economic performance could even enhance the ratings.

The risks facing South Africa’s economic future are both immediate and structural. The energy crisis remains the single largest drag. Load shedding eased in 2024, but the system remains fragile. Outages returned in early 2025.

Many firms, especially SMEs still lack the capital to build their own backup power, making them especially vulnerable. SOEs remain a fiscal risk.

Entities like Eskom and Transnet need deep governance reform, capital injection, and operational restructuring. If mismanagement continues, these companies could remain a drag on government finances. They might fail to deliver the infrastructure needed for growth

South Africa faces a persistent and severe employment problem, with unemployment rates among the highest in the world. As of 2025, the official unemployment rate hovers around 33%, while youth unemployment exceeds 60%.

Informal employment remains widespread, providing livelihoods but often lacking stability, social protections or career advancement. High unemployment exacerbates inequality and fuels social tensions. It also constrains domestic demand. Therefore, job creation is a central challenge for sustainable economic growth.

South Africa experiences significant human capital flight. Many skilled professionals leave for countries offering better pay, safety, and career opportunities.

This “brain drain” is caused by high crime rates. It is also due to political instability, slow economic growth, and limited prospects in the domestic labor market.

The loss of talent hampers productivity. It reduces innovation and weakens critical sectors. This situation makes it a persistent challenge for the country’s long-term economic development.

Corruption and weak institutional capacity also pose major risks. Without credible institutions, investor confidence will remain fragile, and reform momentum could stall.

The country has a very high ratio of social benefit recipients to taxpayers. Since 1994, social spending has been heavily directed toward black households. Today, black South Africans receive roughly 80% of government transfers while contributing around half of total taxes.

The transition to a greener global economy presents both opportunities and risks. If South Africa fails to modernize its mining sector, it could be left behind. This is especially true as demand for green metals surges.

Strengths and Long-Term Opportunities

South Africa’s economy stands out for its strong and diverse foundations. It is one of the most diversified economies on the African continent. The country has well-developed sectors in mining, manufacturing, finance, agriculture, tourism, and services.

The country has an abundance of natural resources. These include gold, platinum, diamonds, coal, and other rare minerals. This wealth continues to be a major economic driver.

It is also a key attraction for global investors. This rich resource base has also helped build a sophisticated mining industry with world-class expertise.

Another major strength is South Africa’s advanced financial sector. Johannesburg hosts one of the largest and most developed stock exchanges in the world. Stable banking institutions and sound regulatory frameworks support it.

The country also benefits from strong physical infrastructure. It includes an extensive network of highways, rail systems, and modern ports. These facilitate efficient trade and logistics. Its energy and telecommunications infrastructure are among the best in the region.

South Africa’s workforce is comparatively skilled. This is particularly true in technical, engineering, and financial fields. This expertise supports the country’s industrial and service sectors.

The nation serves as a strategic gateway. It provides a strong base for companies seeking access to the rest of Africa and their regional operations. The growing technology, renewable energy, and automotive sectors further enhance South Africa’s long-term economic potential.

Target Corporation has grown from a single discount store into one of the most iconic retail brands in the United States.

Illustration 1: The iconic Target Bullseye Logo

Known for its signature red logo and “Expect More. Pay Less.” philosophy, Target has become a favorite destination for millions of shoppers who value style, convenience, and affordability. From groceries to fashion, home goods to electronics, Target has it all.

From its Minneapolis headquarters, Target manages hundreds of stores across the United States, a sophisticated e-commerce platform, and a growing network of fulfillment and distribution centers.

Its guiding philosophy of blending affordability with style and quality has helped it carve out a unique position in retail.

Unlike traditional retailers that grew cautiously, Target expanded strategically. It focused on curated product offerings. It also emphasized smart store locations and innovative marketing.

By integrating online and offline shopping experiences, Target continues to capture the hearts and wallets of millions.

History

The Target story began in 1962, when George Dayton’s Dayton Company opened the first Target store in Roseville, Minnesota.

From the start, Target differentiated itself from competitors by offering a higher-quality shopping experience at affordable prices.

During the 1970s and 1980s, Target expanded steadily across the Midwest. It also expanded in the Southern United States. The focus was on locations that allowed it to serve growing suburban communities.

Unlike discount chains that competed purely on price, Target invested in store design. It also focused on product quality and customer experience. As a result, it earned a loyal following among middle-class Americans.

In the 1990s, Target introduced its SuperTarget stores, combining general merchandise with full grocery sections. This move positioned Target as a one-stop-shop for families, directly challenging Walmart’s dominance in grocery and household essentials.

Target’s expansion has always balanced growth with brand identity. While Walmart pushed for sheer scale, Target cultivated a reputation for style, design, and a curated shopping experience.

In recent years, Target has also embraced digital transformation. Its e-commerce operations, delivery services, and membership programs help it compete with online giants like Amazon.

Today, Target operates over 1,900 stores nationwide. It employs hundreds of thousands of team members. The company continues to grow its online marketplace and attracts millions of customers every week.

Operations

Nationwide Presence

Target generates revenue through a diverse mix of product categories and services. It blends its physical retail operations with a rapidly expanding digital presence.

The company’s core revenue comes from general merchandise, including apparel, home goods, electronics, and beauty products. Its private-label brands, such as Goodfellow & Co. and Up & Up, allow Target to offer stylish, high-quality products at competitive prices. This strategy creates strong customer loyalty and results in higher margins.

Groceries and everyday essentials are another key revenue driver. SuperTarget and traditional Target locations provide fresh produce, packaged foods, and household staples. This segment not only drives foot traffic but also encourages larger shopping baskets.

E-commerce has emerged as a critical growth engine for Target. Its online platform integrates traditional retail with innovative delivery options, including curbside pickup, same-day delivery through Shipt, and a seamless digital marketplace

Membership and loyalty programs, especially Target Circle, enhance revenue. They offer personalized deals, rewards, and promotions. These incentives drive repeat purchases. These initiatives have allowed Target to capture convenience-oriented shoppers. They also capture value-conscious shoppers. This positions Target as a hybrid retailer that thrives across channels.

Target’s Supply Chain

Target’s supply chain is one of its most critical competitive advantages. The company uses strategically located distribution centers and centralized procurement. It has an advanced logistics network. This setup moves goods efficiently from suppliers to stores and directly to customers.

Its sophisticated inventory management systems reduce waste. They maintain stock accuracy and keep pricing competitive. Its private trucking fleet ensures timely delivery across the country. B

Illustration 6: A target Truck.

By combining technology, scale, and operational discipline, Target’s supply chain supports both its physical stores and e-commerce operations. This combination enables the company to offer convenience and reliability that few competitors can match.

Key Competitors

Target operates in a highly competitive retail landscape. Walmart is its most formidable rival. It leverages unmatched scale and a vast grocery footprint. Walmart’s low-price leadership captures a broad segment of everyday shoppers.

Walmart’s aggressive pricing and expansive store network create constant pressure on Target, particularly in mass merchandise and grocery categories. Please see our article for more information about Walmart: Walmart: Stock Analysis (Nov. 2025) – Insightpost %.

Online retail adds another layer of competition. Amazon has reshaped consumer expectations around convenience, delivery speed, and product variety, directly challenging both Target’s digital and physical offerings.

Amazon’s dominance in e-commerce is significant. Its expanding footprint in grocery delivery poses a continuous threat. This forces Target to innovate across its online channels and fulfillment capabilities.

Membership-based retailers such as Costco present another form of competition. By offering bulk products at discounted prices, Costco attracts cost-conscious, loyalty-driven shoppers, directly challenging Target.

Similarly, Dollar General and Dollar Tree continue to expand aggressively in smaller, value-focused markets. They target regions and segments where Target’s larger-format stores may not fit.

Traditional grocers like Kroger, Albertsons, and Publix also compete with Target’s SuperTarget locations in fresh foods and groceries. Meanwhile, global retailers such as Aldi, Lidl, and Carrefour apply additional pressure. They use regional expertise, low-cost strategies and increasingly sophisticated digital tools.

Illustration 8: Carrefour cheese section

Competitive Advantages

Target’s strongest advantage lies in its brand identity. Unlike Walmart, which prioritizes scale and the lowest possible prices, Target has built a reputation around style. It focuses on an elevated shopping experience.

Technology and operational efficiency are central to Target’s advantage. The company has made significant investments in e-commerce, fulfillment, inventory management, and automation.

Its growing network of micro-fulfillment centers and advanced inventory tracking allow Target to process orders quickly. Integrated digital systems ensure accuracy. Customers receive their products with speed and convenience.

Target’s nationwide distribution network and strategically placed store footprint further enhance its efficiency. Products move rapidly from suppliers to stores. They are delivered directly to customers. This is supported by a logistics system that rivals the best in retail.

See next page for Stock analysis,

Stock Analysis

In this section we will analyze Target’s stock to see if it is a good stock to buy or not. Our philosophy is value investing meaning that we try to find good quality companies that are undervalued. However, we will give a holistic overview. This allows all kinds of investors with different philosophies to judge the stock for themselves.

Revenue and Profits

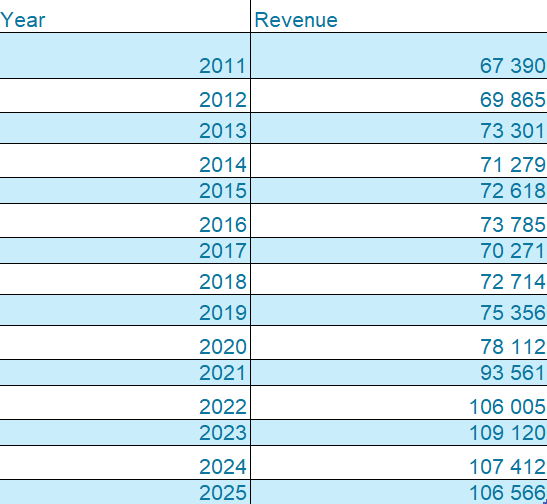

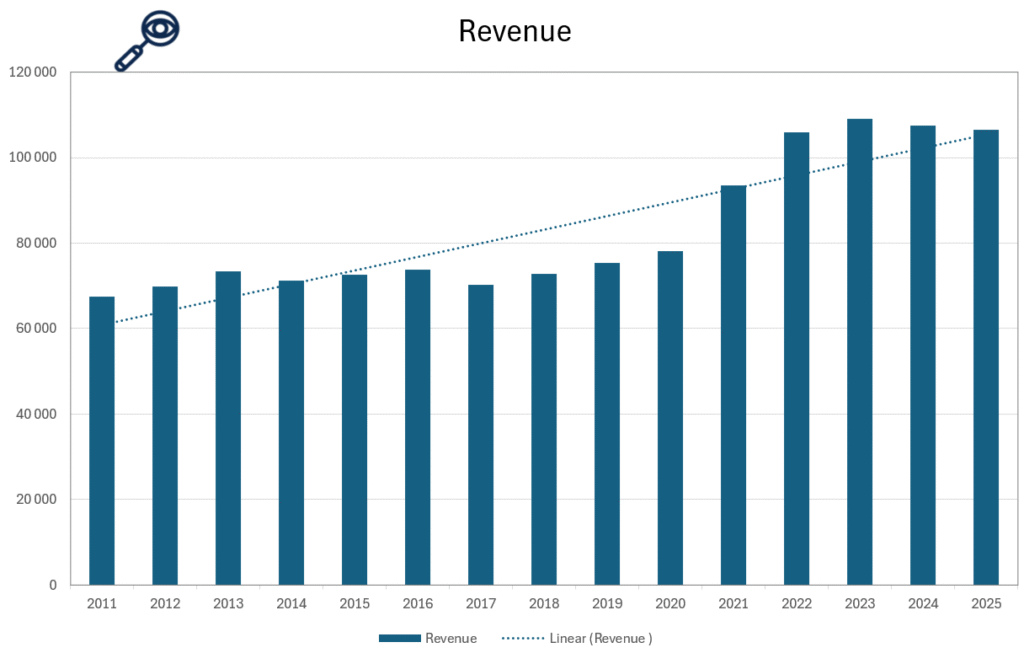

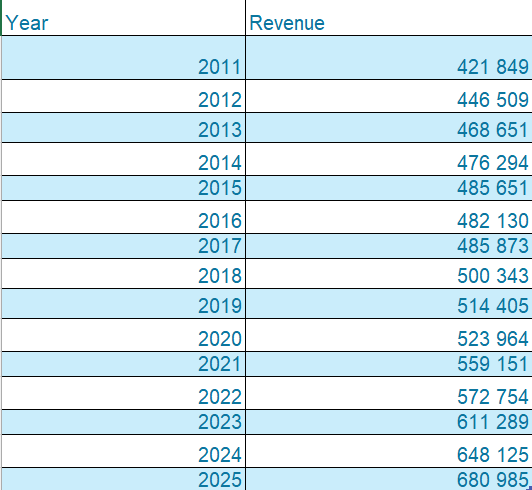

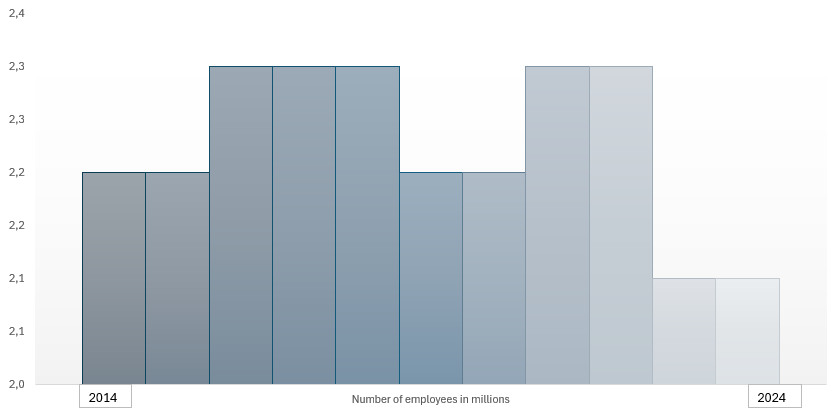

Illustration 9 and 10: Revenue of Target from 2011 to 2025

As shown in Illustrations 9 and 10, Target’s revenue has experienced significant fluctuations over the years. From 2011 to 2020, revenue mainly stayed around the same level. This period reflects stagnation and can be considered a negative signal for consistent growth. The overall trend from 2011 to 2025 has been positive. However, recent data from 2022 to 2025 show that Target continues to experience volatility. Revenue is rising and falling rather than steadily increasing.

Target’s revenue performance between 2015 and 2017 was impacted by various factors, including heightened competition in the U.S. market and operational adjustments in certain underperforming segments, which temporarily suppressed earnings growth.

Overall, while Target has achieved long-term growth from 2011 to 2025, the recurring fluctuations indicate areas of inconsistency. This suggests that investors should be aware of the company’s cyclical performance when considering its stability and long-term prospects. The fluctuation is a red flag that the company has a hard time achieving steady growth.

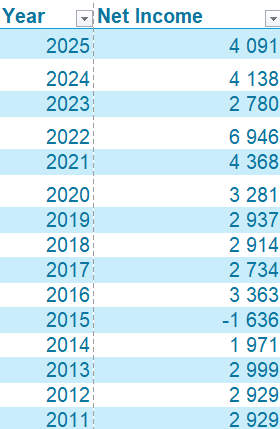

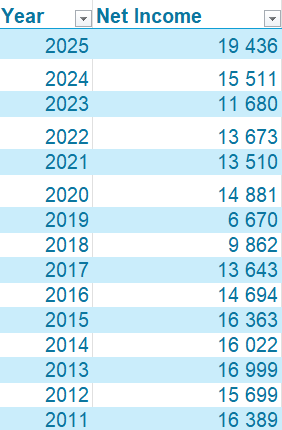

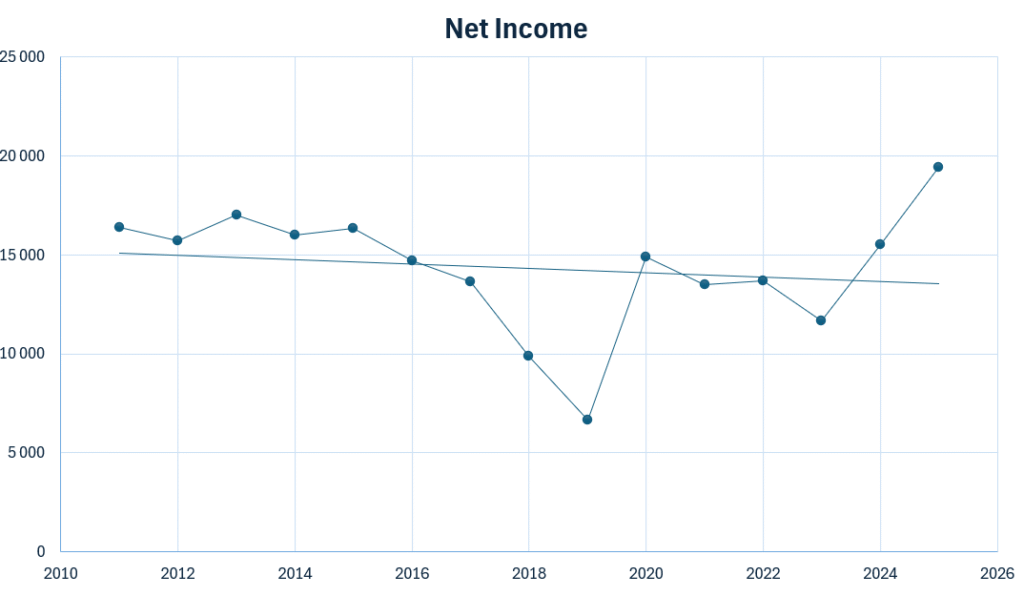

Illustration 11 and 12: Net Income for Target from 2011 to 2025

Net income is a crucial metric to evaluate when determining whether a company is a worthwhile investment. It represents a company’s net profit or loss after accounting for all revenues and income items. All expenses are deducted to calculate the net income as Net Income = Revenue – Expenses.

For Target, as illustrated in figures 11 and 12, several concerning trends appear in the development of net income. The decline in net income from 2011 to 2015 is a clear red flag. It signals operational and strategic challenges during those years. Rising operational expenses affected this period. Competition intensified significantly. The costly impact of Target’s unsuccessful Canadian expansion placed considerable pressure on profitability.

The net income remained flat between 2016 and 2020. There was no meaningful growth during this period. This lack of growth is also a negative sign. A prolonged lack of upward movement suggests stagnation in earnings. This is despite significant investments in digital transformation, store renovations, and supply-chain improvements.

The decline in net income from 2022 to 2023 is another notable warning signal. This drop was largely driven by sharp increases in freight, transportation, and inventory-related costs. Heavy markdowns were also a factor as Target attempted to correct excess inventory. Most significantly, the negative net income in 2015 marks a major red flag. Rising operating costs, margin compression, and persistent competitive pressure have culminated. This move into negative territory reflects these challenges.

Overall, Target’s net income trend raises concerns. The repeated declines (2011–2015 and 2022–2023), the prolonged stagnation (2016–2020), and the negative net income in 2015 collectively indicate that Target has faced significant profitability challenges. Persistent fluctuation without sustained growth is generally a negative sign for long-term financial health.

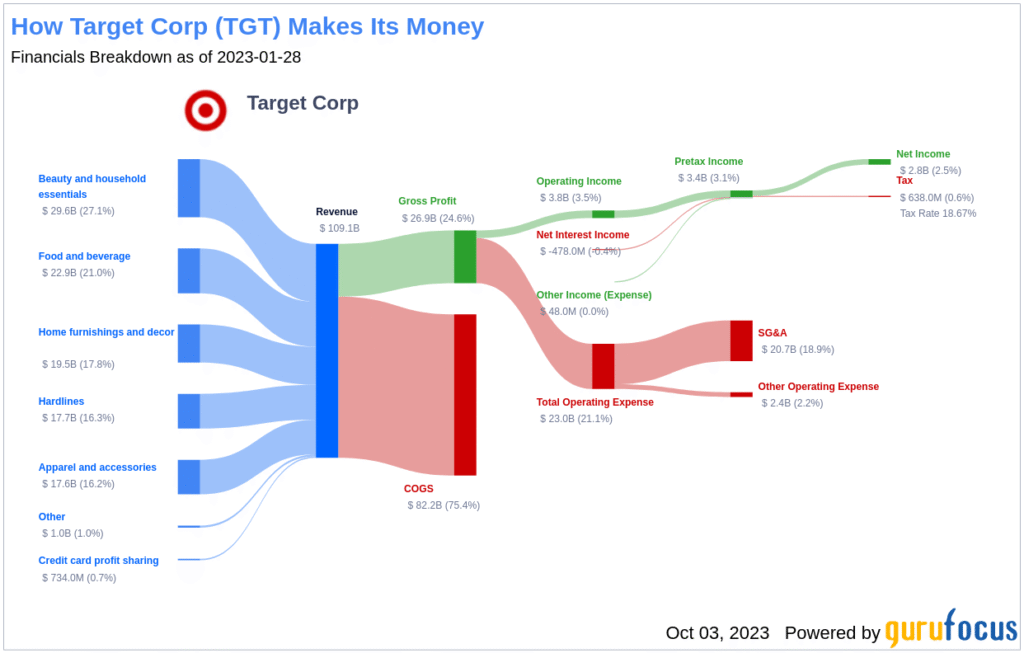

As shown in Illustration 13, Target’s revenue is driven primarily by its U.S. retail operations, as the company operates exclusively within the United States. Essentials & Beauty represents Target’s largest and most stable revenue contributors (around 27%). This category includes household essentials, personal care, cleaning supplies, and beauty products. Because these goods are purchased frequently, this segment provides Target with a reliable baseline of recurring revenue.

Food & Beverage is another major driver, accounting for around 21% share of overall revenue. . Although margins in grocery tend to be lower than in discretionary categories, the steady demand improves store traffic. Apparel & Accessories is one of Target’s historically strong segments and a key differentiator from many other big-box retailers. Target’s private-label apparel brands, combined with affordable pricing, drive strong seasonal demand. However, this category can be sensitive to shifts in consumer spending during inflationary periods. It can also be sensitive during recessionary periods. These conditions can lead to volatility.

Home contributes meaningfully to total revenue (17.8%) but has experienced fluctuations in recent years. After strong performance during the pandemic, demand softened as consumers shifted spending toward services and essentials. This cyclicality makes the Home category more volatile than Target’s other segments. Hardlines, which includes electronics, sporting goods, and toys, accounts for a smaller but still important portion of Target’s revenue. Performance in this segment tends to vary with product cycles and holiday-driven demand. Electronics, in particular, can generate high sales volatility depending on consumer trends and promotional activity.

On the cost side, cost of sales typically consumes a large share of Target’s revenue. This reflects the retailer’s competitive pricing strategy in a low-margin environment. Operating expenses, primarily wages, supply-chain costs, digital-fulfillment expenses, and ongoing store investments—make up most of the remaining cost base.

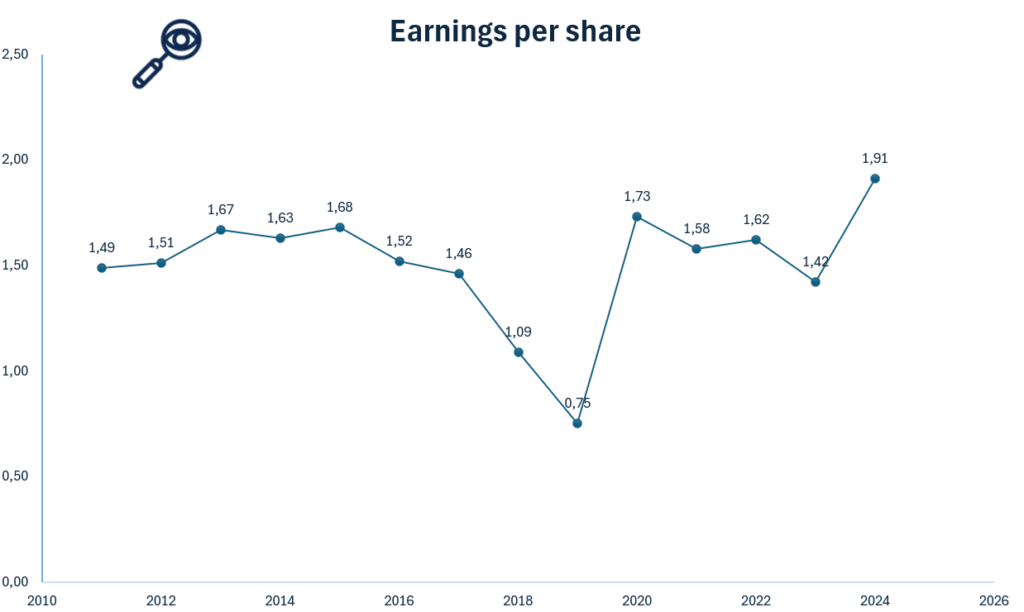

Earnings per share (EPS)

Illustration 14: EPS for Target Corp. from 2011 to 2025

Earnings Per Share (EPS) is a key financial metric. It shows how much profit a company generates for each outstanding share. It is a strong indicator of profitability, financial health, and long-term value creation. While the absolute EPS number matters less to value investors, the trend in EPS is crucial. A steadily rising EPS signals consistent profit growth and a strong underlying business.

For Target, the decline in EPS from 2013 to 2015 is a clear warning sign. This drop was largely driven by the company’s failed Canadian expansion, which resulted in significant operating losses, high exit costs, and considerable write-downs. These challenges placed heavy pressure on profitability and reduced Target’s earnings on a per-share basis.

The second notable dip, from 2022 to 2023, is also concerning. This decline reflects a combination of sharply rising supply-chain and freight costs, inventory costs and broader inflationary pressures. These factors strained margins and negatively affected earnings, even though revenues remained solid.

However, despite these dips, the overall long-term trend in Target’s EPS is positive. When viewed over a longer time horizon, EPS has generally moved upward. This is supported by strong private-label performance. More efficient store operations have also contributed. This upward trajectory suggests that Target has been able to recover from short-term setbacks and continue creating value for shareholders.

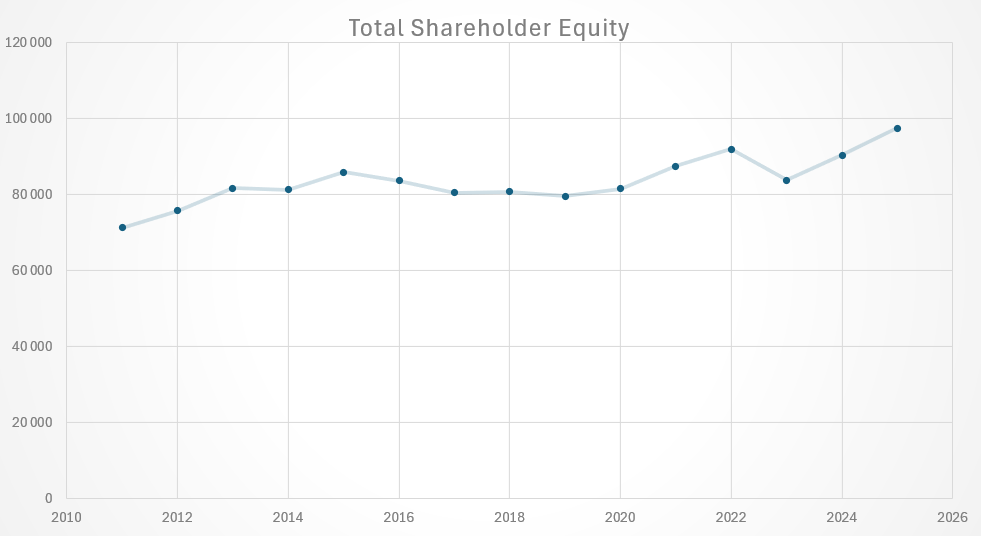

Assets and Liabilities

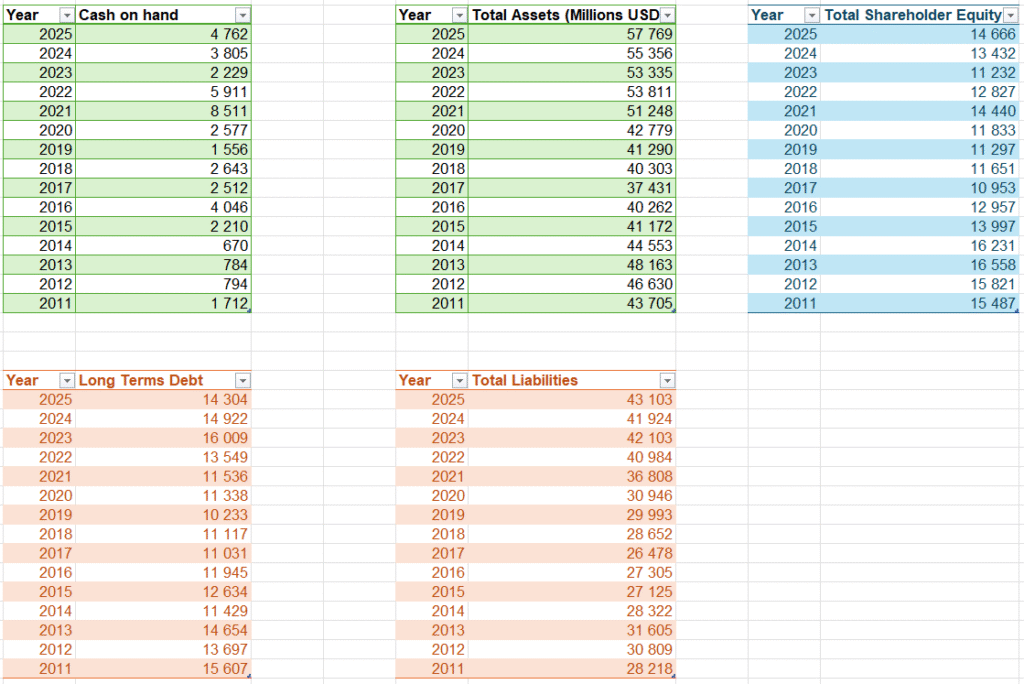

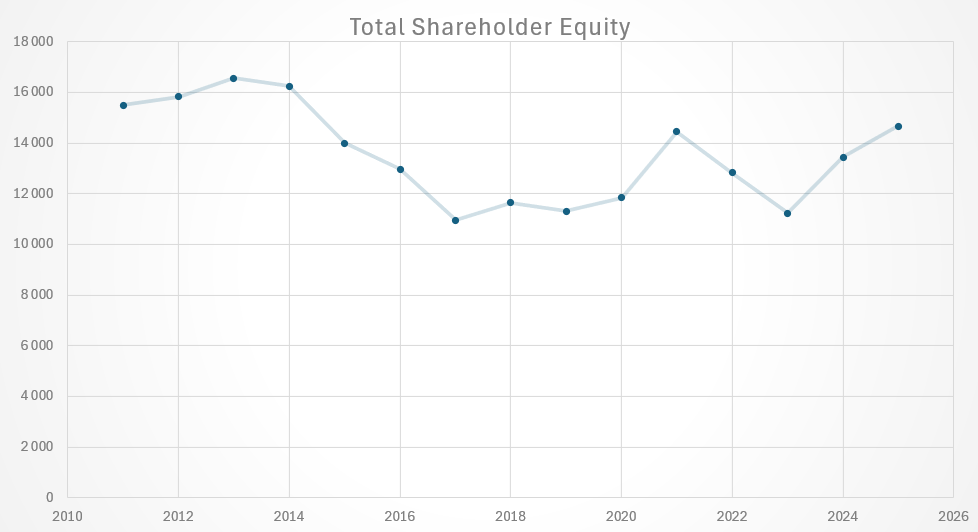

Illustration 15 and 16: Assets and Liabilities for Target from 2011 to 2025

When evaluating a company as a potential investment, understanding its assets and liabilities is essential. Just as you would assess the equity and assets of a local business before considering a purchase, the same logic applies. This also holds true when analyzing publicly traded companies like Target.

As shown in Illustrations 15, the downward trend in shareholder equity is the most concerning element. A declining equity base is a clear red flag, as it suggests that liabilities may be growing faster than assets. Illustration 15 shows that both total liabilities and assets have grown over time. However, assets are growing more slowly than liabilities. This can result from higher operating costs, inventory write-downs, margin pressures, or share buybacks exceeding retained earnings. Regardless of the specific cause, a sustained decline in equity weakens the company’s financial foundation. It reduces long-term value creation for shareholders.

The growth in Target’s total liabilities can also reflect investments in logistics, technology, inventory management and store modernization. Rising liabilities are not inherently negative, but they become more concerning when viewed alongside Target’s fluctuating cash on hand. Instead of showing a steady increase, cash levels have moved up and down year-to-year, signaling inconsistent liquidity management. More importantly, cash on hand is much lower than Target’s long-term debt. This creates a liquidity imbalance. It limits financial flexibility. It also increases reliance on external borrowing. This is a notable risk factor for investors.

Overall, Target’s balance sheet presents both strengths and significant caution points. Asset growth and ongoing investment in operational capabilities are positive. However, the decline in shareholder equity is a worrying sign. Fluctuating cash levels also raise concerns. Additionally, the large gap between cash on hand and long-term debt is something that investors should monitor closely.

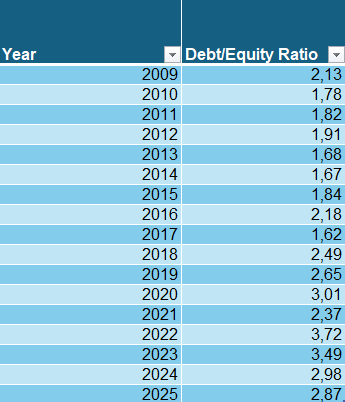

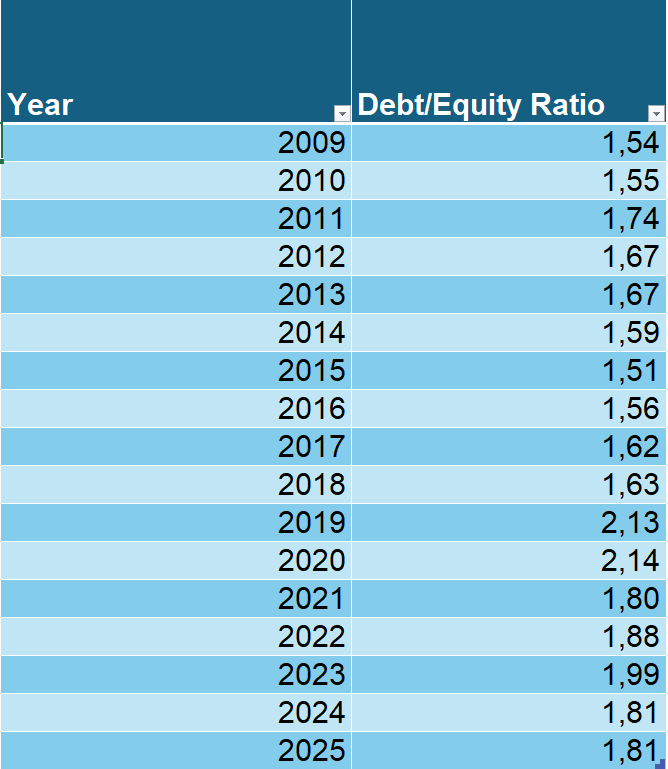

Debt to Equity Ratio

Illustration 17 and 18: Debt to equity ratio for Target from 2011 to 2025

The Debt-to-Equity (D/E) ratio is a key metric for assessing a company’s financial leverage and risk. It measures how much debt a company uses to finance its operations relative to shareholder equity. A higher D/E ratio indicates greater reliance on debt. This reliance can increase financial risk. This is especially true during economic downturns when meeting debt obligations becomes more challenging. Conversely, a lower D/E ratio suggests the company is primarily equity-financed, reducing risk but potentially limiting rapid growth opportunities.

Legendary value investor Warren Buffett generally prefers a debt-to-equity (D/E) ratio below 0.5. Walmart’s D/E ratio, however, stood at approximately 2.81 in 2025. For Target, the D/E ratio has shown a concerning upward trend over recent years, as can be seen in illustration 18. This rise indicates that Target is increasingly relying on debt to fund operations, store remodels, digital investments, and inventory management. While debt can accelerate growth, the steady increase in leverage is a negative sign. It exposes the company to higher financial risk if profitability or cash flow were to weaken.Target is gradually becoming more leveraged. Investors should monitor this situation closely. Continued increases in debt relative to equity could limit financial flexibility. They could also heighten vulnerability to economic shocks.

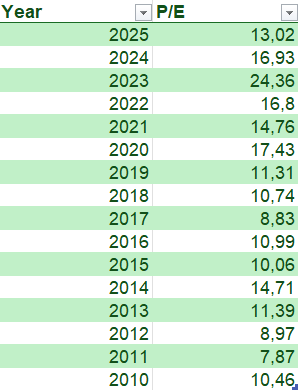

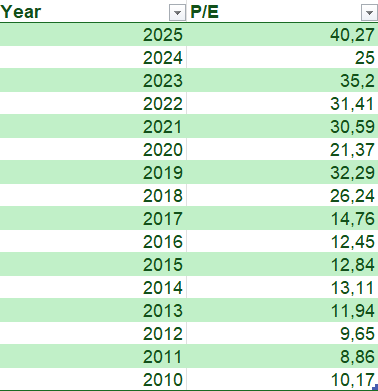

Price to earnings ratio (P/E)

Illustration 19 and 20: P/E Ratio of Target from 2010 to 2025

For value investors, one of the most critical metrics when evaluating Walmart’s stock is the price-to-earnings (P/E) ratio, as it helps assess whether the company is undervalued or overvalued. Even if a company has strong financials, purchasing its stock at a high price can lead to poor returns. For example, imagine a business generating solid profits of $1 million per year. If the owner offers to sell you the business for just $1, it would be an incredible deal. But if the owner asks for $1 trillion, even though the business is profitable, the price would be absurdly overvalued. The stock market works similarly, companies can be priced cheaply on some days and excessively expensive on others.

Warren Buffett, a legendary value investor, typically considers stocks with a P/E ratio of 15 or lower as “bargains.” A high P/E ratio suggests that investors are paying a premium for the company’s earnings, expecting significant growth.

Target’s P/E has declined significantly in recent years. In 2023, it was around 24.36x, and as of 2025 it sits at about 13.02x, reflecting a substantial drop. This recent decline brings the stock back in line with its historical average P/E. Historically, it has generally ranged from 10x to 14x. Therefore, it is fairly valued from a long-term perspective.

The drop in P/E largely reflects a decrease in earnings per share (EPS). Target’s EPS fell from $14.10 in 2022 to $5.98 in 2023, which pressured the stock’s valuation and investor sentiment. The lower P/E indicates that the stock is no longer trading at a high premium. It also reflects recent earnings volatility. The challenges Target has faced include margin pressures, higher operating costs, and inventory management issues.

From a value-investor standpoint, the current P/E suggests that Target is now reasonably valued. The stock may even be modestly undervalued compared with both its recent peak and historical levels. This presents a potential entry point for long-term investors who believe the company can stabilize and grow earnings again. However, caution is warranted, as continued earnings volatility or macroeconomic pressures could make the stock less attractive. Overall, the recent dip in valuation makes Target’s stock more appealing than it has been in recent years. This aligns the price with its earnings. It creates a better opportunity for value-oriented investors.

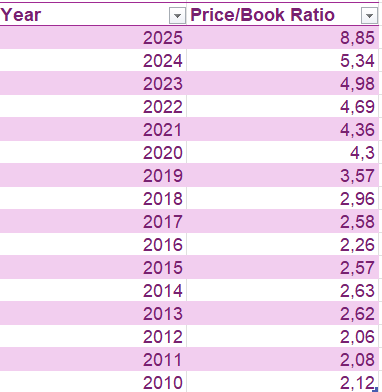

Price to Book Value (P/B)

Illustration 21 and 22: Price to book value of Target from 2010 to 2025

The price-to-book (P/B) ratio compares a company’s market valuation to its book value. It essentially measures how much investors are paying for each dollar of shareholder equity. A lower P/B ratio can indicate that a stock is undervalued. This means investors are paying less for the company’s assets than they are actually worth. Conversely, a high P/B ratio suggest overvaluation or reflect investor expectations of strong future growth. This metric is often used by value investors to assess whether a stock is trading at a fair price relative to its underlying assets.

For Target, the recent decline in the P/B ratio from around 8.72x in 2022 to approximately 2.58x in 2025 is significant. This sharp drop largely reflects the company’s declining earnings. It also reflects shareholder equity pressures during this period. The pressures are driven by margin compression, higher operating and supply-chain costs, and inventory challenges. The drop was initially a warning sign. Now, the resulting low P/B suggests that Target is trading well below its historical valuation levels. This makes the stock appear undervalued from a value-investor perspective.

At the current P/B of roughly 2.58x, the stock is much closer to the range typically favored by value investors, such as Warren Buffett, who often seeks P/B ratios near or below 2x. This indicates that the market is pricing Target’s shares more in line with the company’s actual assets, rather than speculative growth expectations. The recent dip has stemmed from operational and margin pressures. However, it has created a potential opportunity for long-term investors. Now, the stock is trading at a discount relative to its book value and historical norms.

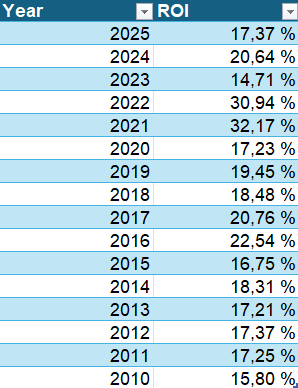

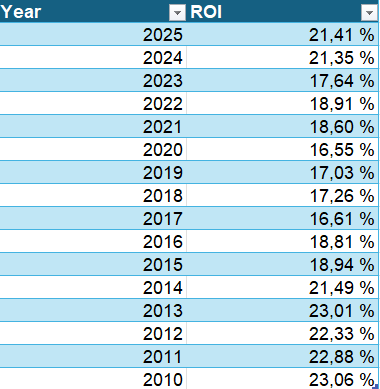

Return on Investment (ROI)

Illustration 23 and 24: ROI for Target from 2010 to 2025

For value investors, Return on Investment (ROI) is a key metric for evaluating Target, as it shows how efficiently the company is using its capital to generate profits. A strong ROI shows that Targetgenerates solid returns compared to the capital it deploys. This makes Target an attractive investment, even if the absolute revenue numbers are large.

Target’s ROI has historically been modest compared with some of its peers. From 2010 to 2020, ROI hovered around 15–20%, reflecting moderate efficiency in its operations and capital deployment. In 2021, ROI spiked sharply to approximately 32%. This increase was largely due to strong sales growth. Higher margins during the post-pandemic retail boom also contributed. Additionally, effective cost management played a role. This temporary surge highlighted Target’s ability to generate excellent returns when market conditions and operational execution align.

However, this improvement proved short-lived. From 2022 through 2024, ROI declined steadily back to around 15%, driven by rising supply-chain and freight costs, margin pressures from heavy markdowns, and higher operating expenses. These factors significantly reduced the efficiency of Target’s invested capital. The lower ROI underscores that, despite strong revenue, the company has struggled to translate sales into proportional returns on investment.

Overall, Target’s ROI remains relatively low, which is a cautionary sign for investors focused on capital efficiency. While the sharp increase in 2021 demonstrated the company’s potential under favorable conditions, the subsequent decline highlights ongoing operational challenges and the need for careful cost and capital management. From a value-investor perspective, the low ROI suggests that returns on invested capital are limited, even though recent strategic initiatives in supply-chain optimization and digital expansion could help improve efficiency over time.

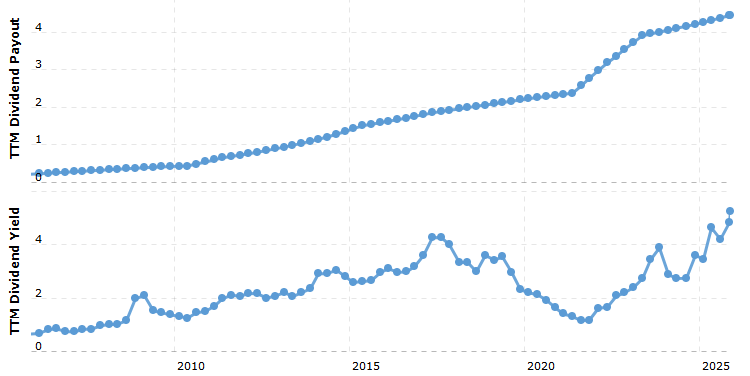

Dividend

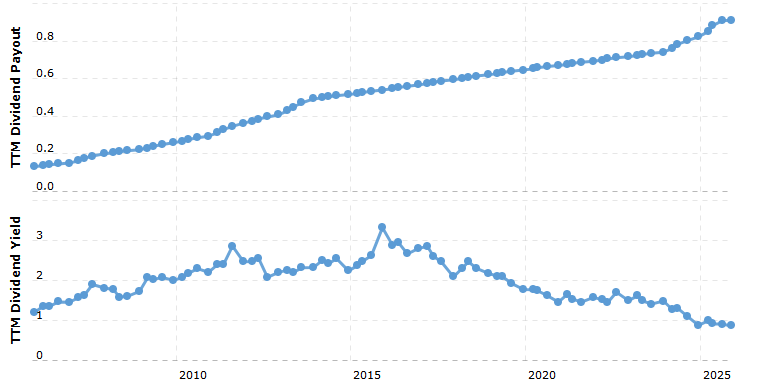

Illustration 25: Target Dividend Yield and dividend payout ratio from 2005 to 2025.

Target currently pays an annual dividend of $4.56 per share, resulting in a yield of approximately 5.45%, with a payout ratio around 55–60%. This moderate payout ratio shows that the dividend is reasonably sustainable. It also allows the company to retain a significant portion of earnings for operational needs, store remodels and inventory management. Additionally, it supports growth initiatives such as digital and supply-chain expansion.

The relatively high yield is attractive for income-focused investors. However, it also reflects some market caution regarding Target’s earnings volatility. Additionally, there have been margin pressures in recent years. Despite this, Target has a long history of consistent dividend payments. It has modest, steady increases. This demonstrates a commitment to returning value to shareholders.

Overall, Target’s dividend profile is a green flag. The dividend is generous and covered by earnings. It provides a reliable income stream. Meanwhile, the company maintains sufficient retained earnings to support ongoing investments.

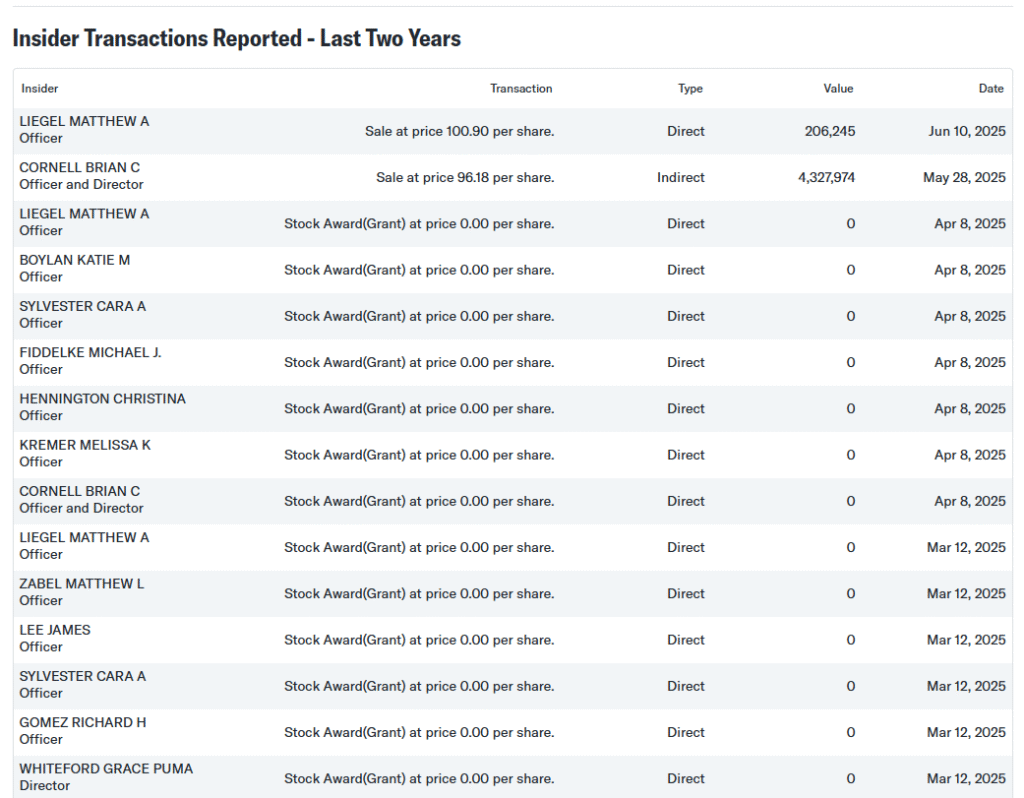

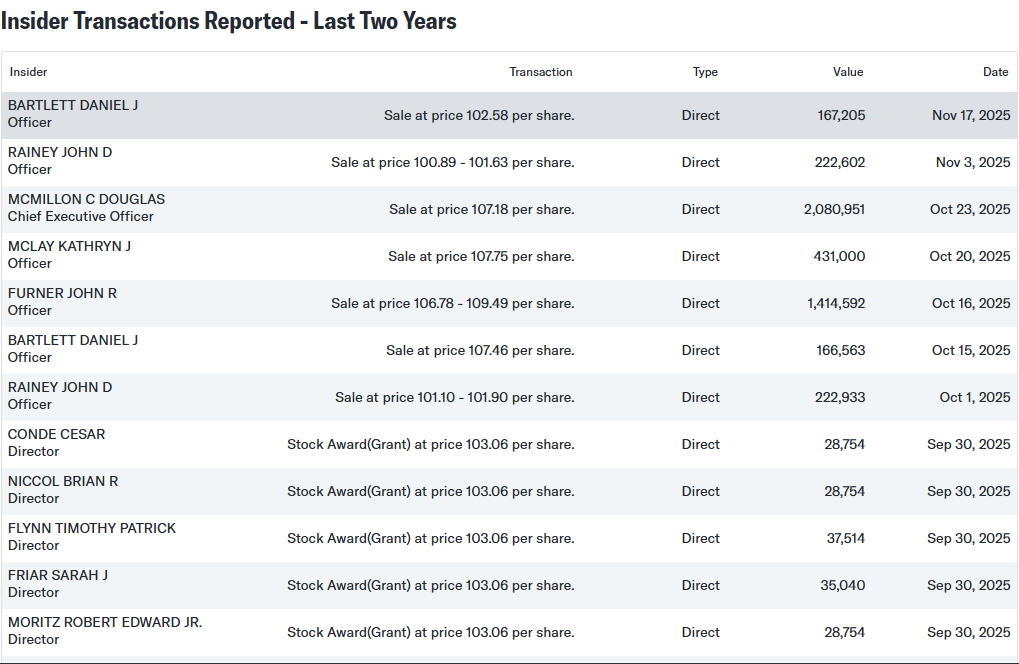

In recent months, Target insiders have sold a significant amount of stock, which can be considered a red flag for investors. CEO Brian Cornell sold approximately 45,000 shares at an average price of $96.18, worth over $4 million. Chief Accounting Officer Matthew Liegel also sold shares during the same period. Most of these sales were conducted under prearranged Rule 10b5‑1 trading plans, which allow insiders to sell shares according to a pre-approved schedule. The scale of these transactions is notable. It could signal that insiders may have concerns about the near-term upside of the stock.

Rule 10b5‑1 plans reduce the likelihood that trades reflect a sudden loss of confidence. Despite this, the combination of large insider sales and relatively modest insider ownership in Target suggests caution. It may indicate that key executives are taking profits while the stock price is elevated, which can be a warning sign for potential investors. Target’s insider trading policy requires trades to occur during open windows and under pre-approved plans, providing governance oversight. However, the recent activity still highlights that insiders are reducing their exposure.

Other Company info

Founded in 1902, Target Corporation is one of the largest and most recognized retail chains in the United States, known for its combination of affordable products, stylish merchandise and growing e-commerce presence. As of 2024, Target employs approximately 450,000 people across its stores, distribution centers, and digital operations. The company is publicly traded on the New York Stock Exchange under the ticker symbol TGT and operates within the Consumer Discretionary sector, specifically in the Retail—Discount Stores industry.

Target is headquartered at 1000 Nicollet Mall, Minneapolis, Minnesota, USA. As of 2024, the company has roughly 496 million shares outstanding, with a market capitalization of around $95 billion USD. For more information, visit Target’s official website: https://corporate.target.com

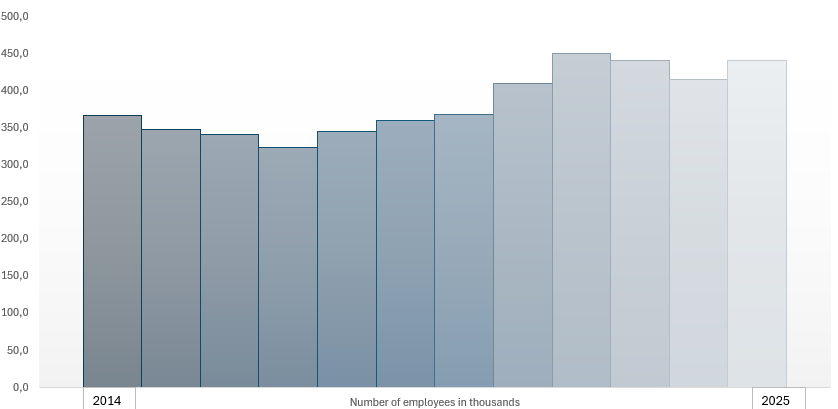

Illustration 27-29: Number of employees and location of Target Corp.

Final Verdict

Overall, Target is not recommended as a value investment at this time. While the stock may appear reasonably priced, recent declines in sales, lowered earnings guidance, its reduced shareholder equity, fluctuating revenue, low ROI, high debt to equity ratio and net income and notable insider selling suggest caution.

Competitive pressures and operational challenges in the retail sector limit upside potential. This situation makes Target a red flag for long-term investors, even though it has a strong brand and solid operations.

Walmart Inc. stands as one of the most powerful and transformative companies in modern economic history. What began as a single discount store in rural Arkansas has grown into the world’s largest corporation. The everyday shopping habits of hundreds of millions of people is influenced by Walmart.

Illustration 1: The Walmart Spark, a symbol that represents affordability, low prices and accessibility.

Walmart is far more than a place to buy groceries or home goods. It is a global entity operating on a scale that few companies in any industry have ever achieved.

From its headquarters in Bentonville, Arkansas, Walmart oversees thousands of stores. It manages massive distribution networks. Walmart has one of the most sophisticated supply chains on Earth.

The company’s guiding philosophy, known as Everyday Low Prices, revolutionized retail by combining relentless cost discipline with unparalleled operational efficiency.

Traditional retailers expanded cautiously. Meanwhile, Walmart pushed forward with aggressive store openings. It engaged in tight supplier negotiations and made investments in logistics technology. These strategies allowed it to dominate markets across the United States.

Today, Walmart operates e-commerce platforms, digital marketplaces, and financial services. It also manages last-mile delivery systems, robotics labs, and one of the world’s largest private trucking fleets. With its increasing emphasis on data, automation and online retail, Walmart continues to redefine the future.

History

The Walmart story began in 1962 when Sam Walton opened the first Walmart Discount City store in Rogers, Arkansas. His core belief was that customers should have access to quality goods at the lowest possible prices. This philosophy set Walmart apart from competitors at a time when discount stores were seen as low-quality alternatives.

Illustration 2: First Wall Mart opened in Rogers, Arkansas

Walton’s approach quickly attracted loyal shoppers, especially in underserved rural areas where Walmart filled a significant retail gap.

During the 1970s and 1980s, Walmart expanded throughout the American South and Midwest. It built a formidable network of stores. This network was supported by a logistics system. This system would become one of its greatest strengths.

Illustration 3: A classical Walmart Store in Englewood, Colo

When the company introduced Walmart Supercenters, it combined general merchandise with full grocery departments. Walmart then became the dominant grocery retailer in the United States. It holds this position overwhelmingly to this day.

The 1990s marked Walmart’s international expansion, beginning with Mexico and Canada followed by ventures into Asia, South America and Europe. Some markets proved challenging. Yet, Walmart’s global presence remains significant. Millions of customers visit its stores and online platforms every day.

The company’s greatest transformation came in the 2010s and 2020s, when it invested heavily in e-commerce through acquisitions such as Jet.com and Flipkart in India and by building its own digital infrastructure to compete directly with Amazon.

Today, Walmart operates over 10,000 stores across multiple continents, employs more than two million people and consistently ranks among the world’s most influential and valuable companies.

Operations

Global Presence

Walmart’s operations span thousands of physical stores in various formats, including Supercenters, Neighborhood Markets, and Sam’s Club warehouse stores. It also runs a rapidly growing international division with strong presences in Mexico, Central America, India, and other regions.

More than 240 million customers visit Walmart stores and websites every week. They rely on the company for groceries, apparel, electronics, home essentials, pharmaceuticals, and countless other products.

The scale at which Walmart operates is staggering. It handles immense volumes of goods from suppliers around the world, manages advanced transportation systems and depends on real-time data. Its U.S. network is vast. Most Americans live within a short drive of a Walmart. This gives the company a unique advantage.

E-Commerce and Digital Transformation

Although Walmart built its empire through physical retail, the company has undergone a dramatic digital transformation over the past decade. It now operates one of the largest e-commerce platforms in the United States. The company is rapidly expanding in online grocery delivery, general e-commerce and third-party marketplace sales.

Walmart’s membership program, known as Walmart Plus, provides customers with fast delivery. It offers fuel discounts and various digital conveniences. These conveniences integrate online and in-store shopping.

The company is also building automated fulfillment centers inside or adjacent to existing stores. They use robotics and machine learning to improve picking speed and reduce costs. This helps fulfill orders within hours.

Walmart employs thousands of engineers, data scientists and technology specialists. They work on advanced inventory systems, artificial intelligence, cybersecurity and cloud architecture. Its growing network of micro-fulfillment centers shows Walmart’s ambition. The company aims to become a digital and technological powerhouse. It wants to rival the world’s leading tech giants.

Supply Chain Dominance

Walmart’s supply chain is often described as one of the greatest business achievements of the modern era.

The company pioneered real-time inventory tracking, satellite-linked store communication and massive automated distribution hubs long before competitors embraced similar technologies.

Its private truck fleet is among the largest in the world. Walmart’s centralized procurement operations allow them to negotiate favorable terms with suppliers. This often influences manufacturing standards, packaging, and pricing across entire industries.

This logistics mastery allows Walmart to move goods efficiently, reduce waste, and keep prices lower than most competitors. The company’s distribution network connects thousands of suppliers to millions of customers with remarkable speed and accuracy. This connection creates a competitive advantage. It has proven extremely difficult for rivals to replicate.

Walmart operates in a highly competitive retail environment, with Amazon as its strongest rival. Amazon leads in e-commerce, cloud services, and digital innovation. In contrast, Walmart excels in physical retail and groceries. This creates an ongoing battle between scale and technology.

Target competes by focusing on curated products and a stylish customer experience, appealing to shoppers who value design.

Costco remains a major force through its membership model and strong loyalty, pushing Sam’s Club to keep improving. Traditional grocers like Kroger and Albertsons challenge Walmart on fresh food and store quality. Global retailers such as Carrefour, Aldi, Tesco and Alibaba leverage regional strength. They also use advanced digital tools.

Dollar General and Dollar Tree add pressure at the extreme value end. They are expanding into areas where Walmart’s larger stores don’t fit. Together, these competitors force Walmart to continuously refine pricing, logistics, and its overall shopping experience.

Competitive Advantages

Walmart’s greatest advantage is scale. Its purchasing power and extensive distribution network allow it to secure low costs and maintain everyday low prices.

The company’s supply chain is supported by automation and AI. Real-time inventory systems also play a role. Together, they make it one of the most efficient in the world.

Walmart has a powerful position due to its nationwide store network. It blends physical stores with services like curbside pickup. It also offers same-day delivery. This reach is difficult for online-only competitors to replicate.